Pritish Bhattacharya

&

Francis E. Hutchinson

ISEAS – Yusof Ishak Institute

Introduction

Since gaining independence 66 years ago, Malaysia has enjoyed rapid economic growth while maintaining a reasonable level of macroeconomic stability. The overall steady trends of most major indicators—including gross domestic product (GDP), inflation, unemployment, and government finance—suggest that the country’s fiscal policy has played a vital role in meeting the development goals of both the public and private sectors.

However, since the beginning of the new millennium, the country’s finances have taken a turn for the worse, with persistent deficit spending and increasing levels of government debt. This has spurred the search for both immediate and long-term fiscal solutions, with the most attention-grabbing measure being the short-lived imposition of the goods and services tax (GST), whose implementation contributed to the toppling of the Barisan Nasional (BN) coalition in 2018. Nonetheless, the pressing need for fiscal reform remains and has been exacerbated by one long-term structural trend—the decline in proportional terms of oil and gas (O&G) related revenue; and one sharp external shock—the COVID-19 pandemic. Thus, at this juncture, Malaysia is even more in need of far-reaching fiscal consolidation measures.

This article comprises five sections. After this introduction, the second section sets out the key aspects of Malaysia’s fiscal policy in recent decades while the subsequent section looks at the key sources of revenue for the Malaysian government and in particular structural trends in the O&G sector. The fourth section analyses the impact of the COVID-19 pandemic, and the concluding section focuses on options for reform going forward.

Background

Colonial Malaysia’s economy relied almost exclusively on the export of primary goods such as tin, rubber, and timber to generate growth. But rapidly declining global commodity prices during the initial few years following independence in 1957 exacerbated rural poverty and unemployment statistics, forcing the government to put its weight behind agricultural diversification and import-substitution-based industrialisation. The adoption of a generally laissez-faire approach to the domestic economy, however, did not give the much-needed boost that policymakers were hoping for. The situation was further complicated by the underlying racial and religious tensions in the country, which culminated in the deadly riots of 1969 (Ungku Abdul Aziz 1970; Wicks 1971; Rönnbäck et al. 2022).

Recognising the hazards of pursuing growth without equity, the government introduced the New Economic Policy (NEP) in 1971. One of the scheme’s most salient features was that state intervention was no longer restricted to the primary sector and rural development, but also encompassed the industrial and commercial sectors. In order to facilitate the rise of Bumiputera (indigenous) enterprises without fostering inequality among other minority ethnic groups, the government spent heavily to acquire corporations from international investors, as well as establish a spate of state-owned enterprises (SOEs) and holding companies in order to accumulate equity. The administration also streamlined taxes and other sources of revenue to fund these formative fiscal interventions (Torii 1997).

The economic restructuring process accelerated dramatically after the discovery of massive oil fields in the country in the 1970s. Although a number of foreign oil giants had been allowed to operate in Malaysia since the early 1900s in return for royalties and tax payments, the combination of the 1973 Organization of Petroleum Exporting Countries (OPEC) Oil Crisis and rising economic nationalism convinced the government to secure greater sovereign control over its O&G resources. This substantial new source of revenue permitted the state to proceed with major subsidies and tariff protection measures without escalating its debt levels in the short run (Gale 1981; Yacob 2021).

It is important to note that the openness of the Malaysian economy made it susceptible to the vagaries of global economic conditions. This was first felt in the mid-1980s, when the country’s oil-fuelled meteoric growth came to a sudden halt after interest rates were cranked up in the U.S., triggering a collapse of world commodity trade. As prices of tin and palm oil—the country’s major exports at the time—nosedived and the demand for manufactured goods plummeted, the prohibitively-priced heavy industry programme that the government had embarked on also slowed down. Additionally, the crashing crude oil prices meant that public borrowing against future oil reserves was not sufficient to run the programme. As government debt ballooned, Malaysia entered into a recession in 1985, with its GDP contracting by 1%. The unforeseen crisis was a tough lesson on the need to rein in the expenditure spree that the government had embarked upon as a means to enhance growth rates (Athukorala 2010).

The recovery phase was marked by greater fiscal discipline, especially in the form of selective privatisation. But the progress was marred by the Asian Financial Crisis (AFC) of 1997–1998. The impact of the Thai baht coming under speculative attack quickly reached the Malaysian ringgit too, whose value took a major hit against the U.S. dollar. With swift outflow of foreign capital, the stock market crashed and companies with foreign-denominated debt began defaulting in quick succession. As the value of non-performing loans (NPLs) climbed, a full-fledged banking crisis ensued. However, the setback was short-lived, and the government managed to pull off a V-shaped recovery through a generous fiscal stimulus package and long-term restructuring of both financial and non-financial institutions (Ariff and Abubakar 1999).

The Malaysian economy fared relatively well in the early 2000s, with an average annual growth rate of 5.5%, at least until the Global Financial Crisis (GFC) of 2008–2009. Due to the highly integrated nature of the country’s financial market, the GFC, which began in the U.S., created giant ripples in the domestic economy as well. Malaysia fell into another recession, with its growth contracting by 1.7% in 2009. But limited exposure to subprime-related assets and another hefty fiscal stimulus package to provide countercyclical support for growth helped cut down the recovery time (Doraisami 2011).

From 2010 to 2019, the economy performed well and relatively consistently, with its annual growth hovering at around 5%. While still very respectable by most standards, this was significantly below the heady days of the late 1980s and early 1990s, when the figure stood closer to 7% per annum (The World Bank 2021). This was not unexpected, given the country’s higher income base and shifting economic model—away from exclusively export-oriented industrialisation to a more diverse economic structure and a greater domestic orientation.

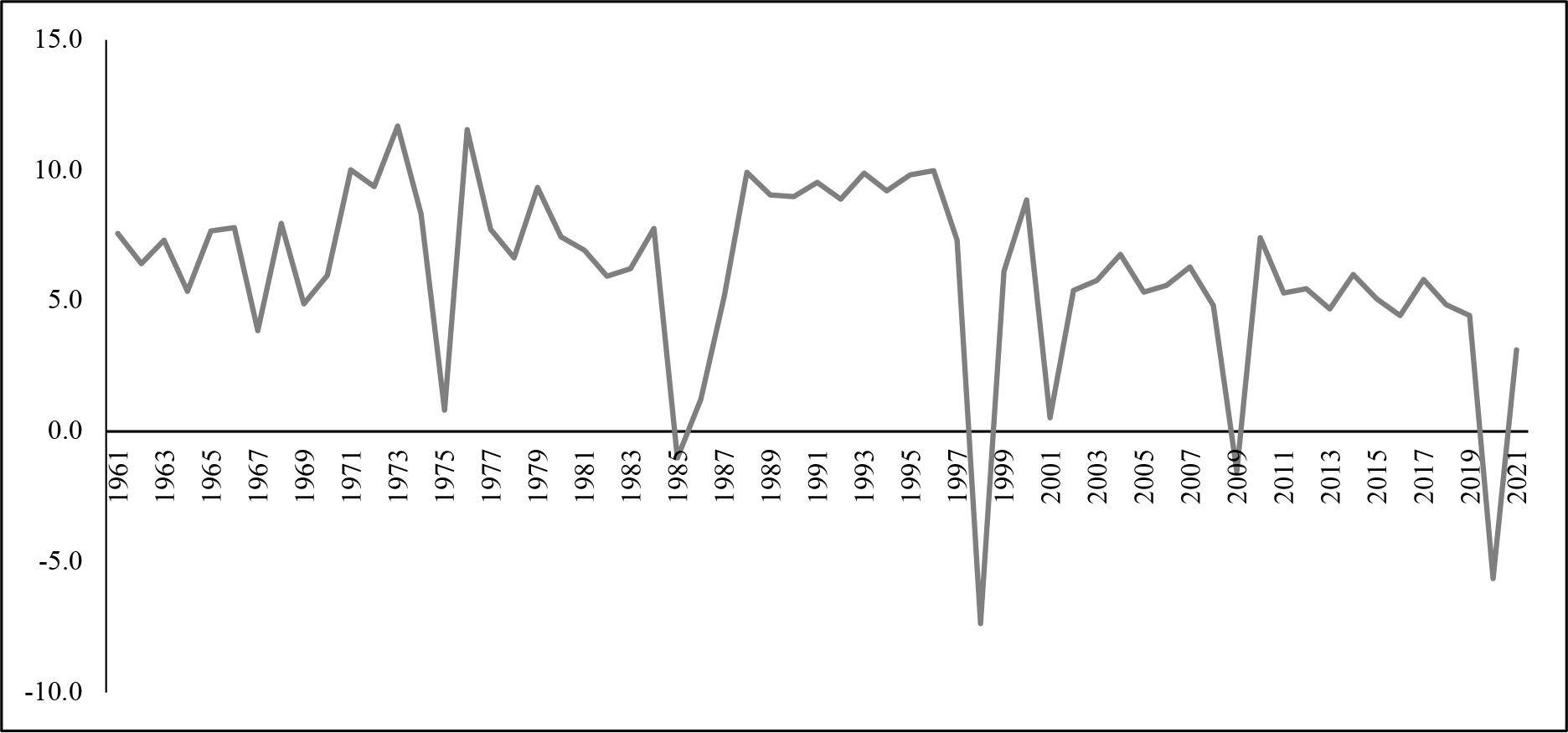

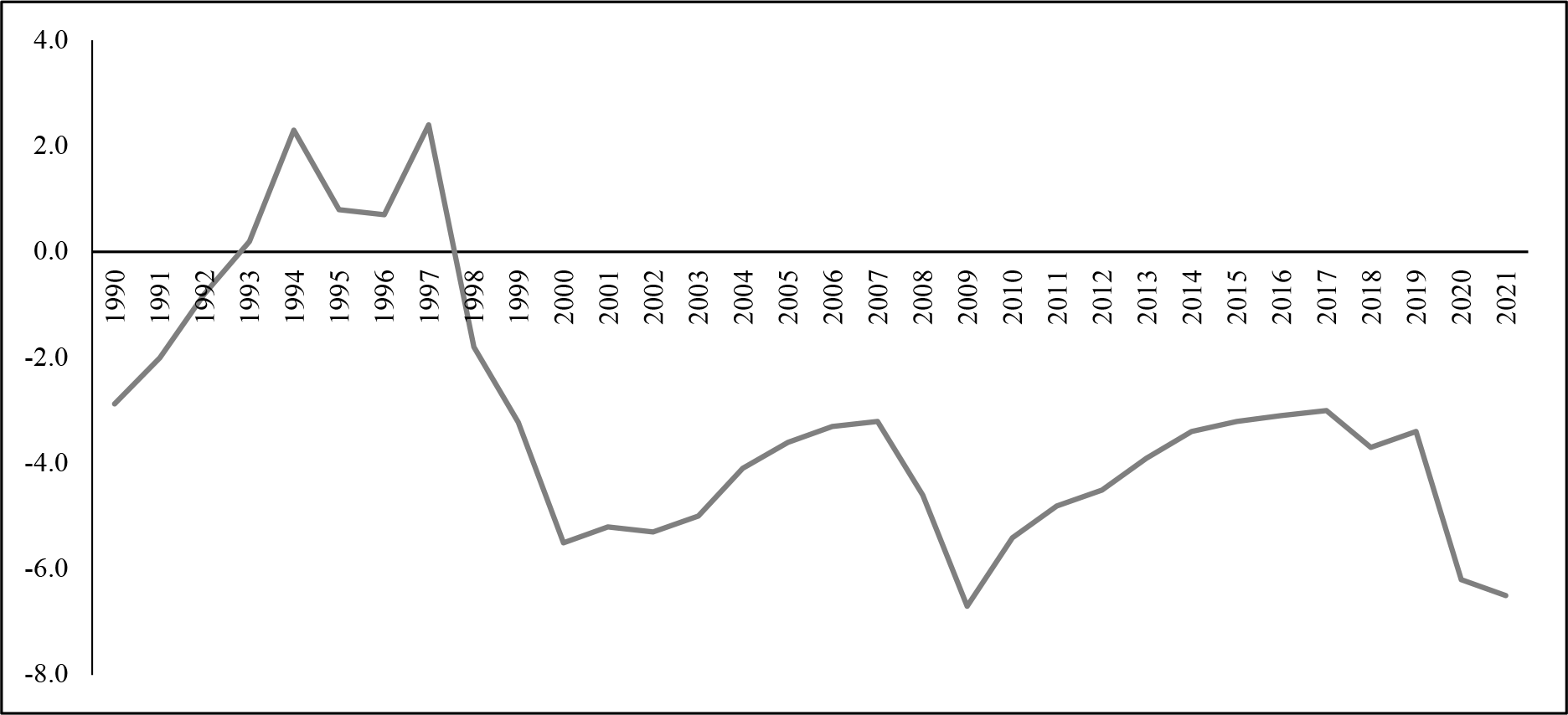

The experience of the past six decades shows that Malaysian lawmakers have relied on a consistent fiscal policy framework to either grow or steady the economy (Figure 1), seamlessly alternating between conservatism and relative profligacy. While this approach has been very successful in stabilising the primary macroeconomic indicators, the consequent continued rise in Malaysia’s government budget deficit (Figure 2) and public debt (Figure 3) cannot be overlooked for long. A rapidly rising budget deficit, from 3.0% of GDP in 2017 to 6.5% in 2021 means that the government will have to borrow more to fund its expenditure, including its debt repayment obligations (Bank Negara Malaysia 2017, 2018, 2019a, 2020, 2021). And the simultaneous increase in the debt ceiling will allow this loop to continue.

For a very long time, Malaysia had conventionally maintained the debt ceiling at 50% of the GDP, raising the level to 55% only in 2009 in response to the GFC. However, when the COVID-19 crisis gripped the nation, the government decided to further increase the limit—first to 60% in August 2020 and then to 65% in October 2021 (Salim 2021). This debt-to-GDP ratio is not as startling as the Japanese or American numbers, it is nonetheless relatively high for an emerging market and significantly above that of comparator economies such as Indonesia, whose debt is a modest 32.3% of GDP (Bank Indonesia 2022).

Figure 1: Malaysia’s annual growth rate (percentage), 1961–2021.

Source: Authors’ creation based on The World Bank (2021) data.

Figure 2: Malaysia’s government budget deficit (as percentage of GDP), 1990–2021.

Source: Authors’ creation based on figures extracted from the CEIC database.1

Figure 3: Malaysia’s government debt (as percentage of GDP), 2002–2021.

Source: Authors’ creation based on figures extracted from the CEIC database.2

The O&G Sector and its Contribution to Government Coffers

Malaysia’s federal government revenue can be sorted under two sources—tax revenue and non-tax revenue—each made up of several components, as shown in Table 1.

Table 1: Malaysia’s federal government revenue sources

| Tax revenue |

Direct tax

|

Indirect tax

|

| Non-tax revenue |

| Licences and permits |

| Investment income |

Source: Authors’ compilation based on the Ministry of Finance Malaysia (2022a) data.

Among the different earning streams, the share of O&G-related revenue stands out. As mentioned in the previous section, since the O&G sector’s take-off in the 1970s, this natural bounty has yielded myriad benefits to Malaysia, proving to be a reliable source of funding for the government’s most ambitious projects. And Petronas, the state-owned corporate giant, holds exclusive ownership rights over all oil and natural gas exploration and production activities in the country. The sector’s fiscal contribution comes in a variety of forms, which are:

- petroleum income tax (PITA) paid by petroleum-related firms;

- royalties from petroleum and gas companies;

- export duties on petroleum products; and

- dividends remitted by Petronas.3

Tables 2 and 3 present the changing composition of O&G revenue over the past 50 years. The first three revenue sources are long-standing. However, since the mid-1980s, Petronas has paid dividends to the Malaysian government. From around 15% in 1985, this has increased to approximately half of the total of petroleum-related revenue in recent years. Consequently, the relative importance of established contributions such as the PITA and petroleum and gas royalty has decreased in relative importance, and the more variable—and more discretionary—Petronas dividend has become the largest source of oil-related revenue over time (Bhattacharya and Hutchinson 2022).

Table 2: Breakdown of Malaysia’s total O&G revenue (in RM million), 1975–1995

| Revenue component | 1975 | 1980 | 1985 | 1990 | 1995 |

| PITA | 322 [80.5%] | 1,736 [63.0%] | 3,130 [49.5%] | 2,644 [35.0%] | 2,185 [32.5%] |

| Petroleum and gas royalty | 78 [19.5%] | 345 [12.5%] | 619 [9.8%] | 627 [8.5%] | 710 [10.5%] |

| Petroleum export duties | 0 | 677 [24.5%] | 1,639 [26.0%] | 1,910 [25.5%] | 751 [11.0%] |

| Petronas dividend | 0 | 0 | 930 [14.7%] | 2,300 [31.0%] | 3,100 [46.0%] |

| Total O&G revenue | 400 | 2,758 | 6,318 | 7,481 | 6,746 |

Note: Percentage in brackets.

Source: Authors’ calculations based on data from figures extracted from the CEIC database.4

Table 3: Breakdown of Malaysia’s total O&G revenue (in RM million), 2000–2020

| Revenue component | 2000 | 2005 | 2010 | 2015 | 2020 |

| PITA | 6,010 [46.7%] | 14,566 [47.2%] | 18,713 [33.8%] | 11,559 [26.5%] | 20,800 [41.0%] |

| Petroleum and gas royalty | 1,763 [13.7%] | 3,293 [10.7%] | 4,900 [9.0%] | 5,142 [11.8%] | 4,300 [8.4%] |

| Petroleum export duties | 996 [7.7%] | 2,029 [6.6%] | 1,745 [3.2%] | 989 [2.2%] | 800 [1.6%] |

| Petronas dividend | 4,100 [31.9%] | 11,000 [35.5%] | 30,000 [54.0%] | 26,000 [59.5%] | 25,000 [49.0%] |

| Total O&G revenue | 12,869 | 30,888 | 55,358 | 43,690 | 50,900 |

Note: Percentage in brackets.

Source: Authors’ calculations based on data from figures extracted from the CEIC database.4

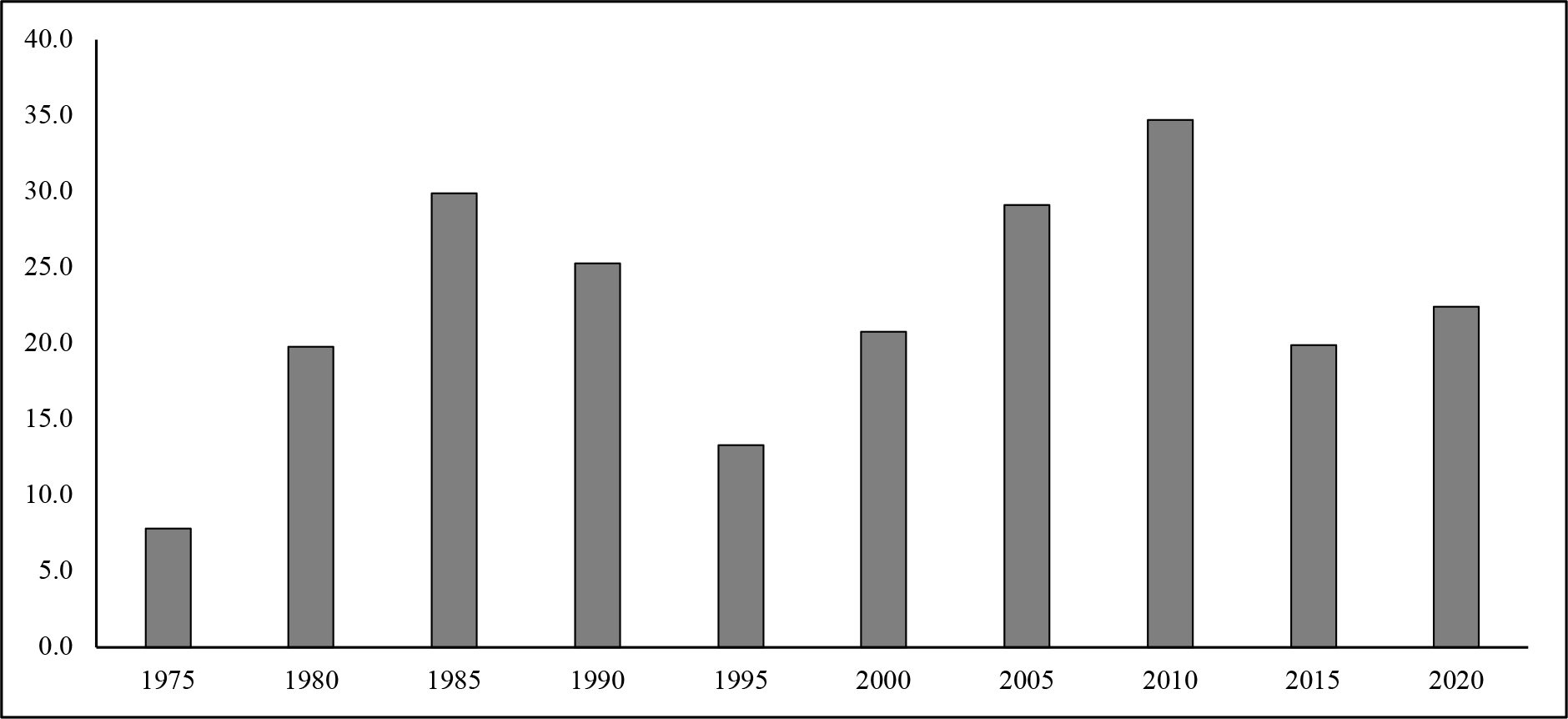

While the O&G sector, together with its substantial derivatives, has undeniably benefited Malaysia, going forward, there are two major challenges facing it. The first concerns the sector’s inconsistent fiscal contribution. Oil prices are influenced by a multitude of supply, demand, and public policy factors—ranging from conventional output decisions made by OPEC or private oil-producing nations to central bank interest rates, or disruptions brought about by natural calamities or political unrest. The global experience over the past three years has shown that unforeseen economic, health, and geopolitical crises can contribute to the variability, too. The issue is further compounded by the cyclicality inherent in oil price movements. The volatility of oil prices significantly affects the government’s fiscal revenue, with price rises adding to the public purse and price crashes depleting it. This fluctuation can be clearly seen in the varying proportion of the revenue derived from the O&G sector in Malaysia’s total government revenue (Figure 4).

Figure 4: O&G revenue as percentage of total government revenue, 1975–2020.

Source: Authors’ calculations based on data from figures extracted from the CEIC database.4

Second, it must be acknowledged that Malaysia’s hydrocarbon resources are not unlimited. The production capacity of the O&G sector in the nation has been on a downward trajectory for some time now, mainly because of maturing large fields. In 2016, total fuel production was 757,000 b/d, while in 2020, this had gone down to 655,000 b/d (British Petroleum 2021). In fact, several studies have tried to determine the precise number of years of oil reserves left in Malaysia. A 2016 estimate claimed that, without net exports, the country would have just enough reserves to last until 2030 (Worldometer 2016). This claim was reinforced in 2019, when the Economic Affairs Ministry announced in parliament that local O&G fields were expected to be depleted by 2029 (Malaysiakini 2019). A slightly more optimistic image emerged in a Petronas report, with records indicating that the national oil reserves would last for 28 years—and 38 if contingent resources were accounted for (Petronas 2019).

The Lingering Impact of COVID-19

The growing levels of budget deficit and government debt, along with the diminishing fiscal contribution of the O&G sector, raise a number of serious questions regarding Malaysia’s long-term macroeconomic stability. The COVID-19 pandemic dealt an unprecedented blow to the economy, and it would be irresponsible to not recognise that this global health crisis exacerbated an already perilous fiscal arrangement.

According to Bank Negara Malaysia, the country’s annual GDP grew by 4.3% in 2019—the lowest rate since the GFC in 2008–2009—and the fiscal deficit reached 3.4% of GDP. The lower-than-expected figures were attributed to shrinking domestic private consumption, and to supply disruptions and lower external demand in light of the worsening trade ties between the U.S. and China (Bank Negara Malaysia 2019b).

When the first few COVID-19 cases were recorded in the country, no one could have predicted the scale and duration of the pandemic’s deleterious effects. However, as daily cases began to be quoted in thousands and then tens of thousands, it became clear that the impact would be deep and long-lasting. The government acted fairly swiftly to contain the spread of the virus, announcing stringent restrictions on mobility and physical contact. The first set of sectors to absorb the immediate impact of the “Movement Control Order” (MCO) included retail, aviation, hospitality, and food and beverage. Several studies have concluded that workers employed in these sectors were disproportionately affected (Yong and Sia 2021; Alamoodi et al. 2022).

In order to save lives and livelihoods during the course of the crisis, the state focused on fiscal injection in the form of various stimulus packages to accompany the cordon sanitaire measures. While some schemes provided direct relief to poor households, others were aimed at assisting small businesses with loans and cash flows. Table 4 presents a summary of the major support measures put in place to deal with the economic fallout of COVID-19.

Table 4: Major economic support packages launched by the Government of Malaysia

| Control measure | Period | Stimulus package |

| Pre-MCO | 27 Feb 2020 – 17 Mar 2020 |

|

| MCO | 18 Mar 2020 – 3 May 2020 |

|

| Conditional MCO | 4 May 2020 – 9 Jun 2020 | |

| Recovery MCO | 10 Jun 2020 – 31 Mar 2021 |

|

| State-level MCOs | 11 Jan 2021 – 31 May 2021 |

|

| Total lockdown | 1 Jun 2021 – 14 Jun 2021 |

|

| National Recovery Plan | 15 Jun 2021 – 31 Dec 2021 |

|

Source: Authors’ compilation based on the Ministry of Finance Malaysia (2022a) data.

Despite the government’s increased fiscal flexibility to mitigate the shocks, individuals who were not covered by the social protection schemes were exposed to job and income losses. Overall, the GDP contracted by 5.6% in 2020, with the primary, secondary, and tertiary sectors all registering negative growth of –2.2%, –2.6%, and –5.5%, respectively. Private final consumption expenditure contracted by 4.3% and exports fell by 12.3%. By the last quarter of 2020, national unemployment had reached a staggering 4.8% (Department of Statistics Malaysia 2021).

Most statistics improved in 2021, but certainly not to pre-COVID levels. For instance, GDP expanded by 3.1%, with manufacturing and services witnessing positive growth (9.5% and 1.9%, respectively). Agriculture, however, continued to contract by 0.2%. Private final consumption expenditure rose by 1.9% and exports by 15.4%. The prolonged effect of the pandemic kept unemployment levels fairly high at 4.6% (Department of Statistics Malaysia 2022).

Preliminary reports highlight that the economy continued to heal in 2022, growing at 5.1% to 5.4%. However, the need to secure a firm grip on fiscal policy is again underscored by the gloomy outlook for this year. With the looming risk of a 2023 global recession on account of the world’s three largest economies—the U.S., EU, and China—stalling, Malaysian policymakers will have to be prepared to simultaneously tackle inflation, unemployment, and inequality (Tay 2022).

Fiscal Reform

The government has been cautious about the deterioration of its fiscal position and plans to pursue fiscal consolidation once the recovery is well established. Particularly, it is crucial to reduce public debt and the contingent liabilities more effectively in the medium term. Considering the low level of tax revenue, this would require comprehensive fiscal consolidation planning that strongly underpins revenue-enhancing measures, in addition to spending reprioritisation and sustainable debt management. In the meantime, because significant downside risks persist, the following targeted policy support measures remain essential:

1. Employing fiscal austerity

Global and local economic uncertainties that have emerged from the U.S.-China trade war, COVID-19, and Russia’s invasion of Ukraine mean that the Malaysian government will have to extend—if not expand—the host of ongoing subsidies for essential goods and price controls to the poor. Funding these expenses without implementing cost-saving measures among government entities is not compatible with the principle of maintaining long-term financial stability for the country. A 2022 circular issued by the Malaysian Treasury titled “Guidelines on Public Expenditure Savings” itself offers an assortment of areas in which statutory bodies can exercise greater fiscal prudence, including operating expenses, appointments, overtime allowance, domestic and overseas accommodation, acquisition of new assets, outsourcing, and development expenditures (Ministry of Finance Malaysia 2022b). These suggestions become even more important given that the country’s public sector wage bill as a percentage of total public sector spending has risen considerably in the past few years. A 2019 World Bank report indicates that this number rose from a low of 17.6% in 2002 to a peak of 29.3% in 2017 (The World Bank 2019).

2. Reining in government-linked corporations (GLCs)

The pervasiveness of Malaysia’s SOEs or government-linked corporations (GLCs) across the private sector, finance, and real estate has put considerable strain on the country’s fiscal capacity. There is also a growing body of evidence to show that GLCs’ special access to public and regulatory agencies and limited public scrutiny present a formidable barrier to both competition and entry of new private firms (see, for instance, Menon and Ng 2017). Not only is the subsequent crowding out of private investment detrimental to economic growth, the federal government’s frequent bailouts of underperforming GLCs are a major drain on the fiscal purse. While successive governments have made regular commitments to reduce mismanagement of and corruption in such public enterprises, the continued dominance of a number of inefficient GLCs must force the government to reassess the extent of its involvement in business.

3. Biting the GST bullet

The GST was a value-added tax, levied at a blanket 6%, introduced in 2015 as an alternative to the sales and services tax (SST). As a broad-based consumption tax, the GST can be used as a major fiscal tool to boost government revenue in the face of dwindling oil reserves and mounting public expenses. The proposed tax regime became a major point of contention among the political parties contesting the 14th General Election, with Pakatan Harapan (PH) vowing to abolish the tax if it came to power. After forming the government in 2018, PH did indeed get rid of the GST and reinstated the SST system, under which the sale of goods attracts a tax of 5% to 10% while services are taxed 6%. Although more popular with the voters, the SST is now proving to be insufficient to generate enough revenue for the state. For instance, GST earnings in 2017 stood at RM44 bn, while the SST amount for 2021 was RM27.9 bn (The Sun Daily 2022). In other words, Malaysia’s current narrow tax base is far from adequate to cope with existing and emerging local and global headwinds.

Conclusion

Malaysia has been blessed with abundant natural resources that have been leveraged to invest in physical and social infrastructure over the past half century. However, the long-term structural decline of this source of income has set in. This has prompted policymakers to consider introducing new sources of income, such as the GST. However, public disaffection led to the introduction of the GST being reversed. While the day of reckoning was temporarily forestalled, the impact of COVID-19 on the country’s finances is a signal that further procrastination in the search for income to strengthen the government machinery and the public services may no longer be an option.

NOTES

1 Retrieved from the CEIC offline catalogue on 19 September 2022. CEIC is a standard international database for macroeconomic, industrial and financial time series for emerging economies.

2 Retrieved from the CEIC offline catalogue on 1 October 2022.

3 There is a fifth source of revenue, namely, income from petroleum operations of the Malaysia-Thailand Joint Authority (MTJA), a body managing petroleum production activities in the Malaysia-Thailand Joint Development Area (MTJDA). However, information on the income from MTJA operations is not available publicly and is therefore not included in the computation of total O&G revenue.

4 Retrieved from the CEIC offline catalogue on 2 October 2022.

REFERENCES

Alamoodi, A. H., Baker, M. R., Albahri, O. S., Zaidan, B. B., Zaidan, A. A., Wong, W.-K., Garfab, S., et al. 2022. Public sentiment analysis and topic modeling regarding COVID-19’s three waves of total lockdown: A case study on movement control order in Malaysia. KSII transactions on Internet and Information Systems 16 (7): 2169–2190. https://doi.org/10.3837/tiis.2022.07.003

Ariff, M. and Abubakar, S. Y. 1999. The Malaysian financial crisis: Economic impact and recovery prospects. The Developing Economies 37 (4): 417–438. https://doi.org/10.1111/j.1746-1049.1999.tb00241.x

Athukorala, P. 2010. Malaysian economy in three crises. Crawford School of Economics and Government Working Paper No. 2010/12. https://crawford.anu.edu.au/acde/publications/publish/papers/wp2010/wp_econ_2010_12.pdf (accessed 1 October 2022).

Bank Indonesia. 2022. Indonesia’s external debt decreased in May 2022. https://www.bi.go.id/en/publikasi/ruang-media/news-release/Pages/sp_2418522.aspx#:~:text=The%20structure%20of%20external%20debt,32.3%25%20in%20the%20reporting%20period. (accessed 1 October 2022).

Bank Negara Malaysia. 2021. Annual Report 2021. https://www.bnm.gov.my/documents/20124/6458991/ar2021_en_book.pdf (accessed 20 October 2022).

____. 2020. Annual Report 2020. https://www.bnm.gov.my/documents/20124/3026128/ar2020_en_book.pdf (accessed 20 October 2022).

____. 2019a. Annual Report 2019. https://www.bnm.gov.my/documents/20124/2724769/ar2019_en_full.pdf (accessed 20 October 2022).

____. 2019b. Economic & monetary review 2019. https://www.bnm.gov.my/o/annual-report/emr-summary.html (accessed 1 October 2022).

____. 2018. Annual Report 2018. https://www.bnm.gov.my/documents/20124/791626/ar2018_book.pdf (accessed 20 October 2022).

____. 2017. Annual Report 2017. https://www.bnm.gov.my/documents/20124/829200/ar2017_book.pdf (accessed 20 October 2022).

Bhattacharya, P. and Hutchinson, F. E. 2022. Malaysia’s oil and gas sector: Constant expectations despite diminishing returns. ISEAS Perspective 2022/21. https://www.iseas.edu.sg/articles-commentaries/iseas-perspective/2022-21-malaysias-oil-and-gas-sector-constant-expectations-despite-diminishing-returns-by-pritish-bhattacharya-and-francis-e-hutchinson/ (accessed 5 October 2022).

British Petroleum. 2021. Statistical review of world energy (70th ed.). https://www.bp.com/content/dam/bp/business-sites/en/global/corporate/pdfs/energy-economics/statistical-review/bp-stats-review-2021-full-report.pdf (accessed 14 October 2022).

Department of Statistics Malaysia. 2022. Malaysia economic performance 2021. https://www.dosm.gov.my/v1/index.php?r=column/cthemeByCat&cat=153&bul_id=UWFBZkhFZDBhanN5ZEUxRS96T2VRdz09&menu_id=TE5CRUZCblh4ZTZMODZIbmk2aWRRQT09 (accessed 17 September 2022).

____. 2021. Malaysia economic performance fourth quarter 2020. https://www.dosm.gov.my/v1/index.php?r=column/cthemeByCat&cat=100&bul_id=Y1MyV2tPOGNsVUtnRy9SZGdRQS84QT09&menu_id=TE5CRUZCblh4ZTZMODZIbmk2aWRRQT09 (accessed 17 September 2022).

Doraisami, A. 2011. The global financial crisis: Countercyclical fiscal policy issues and challenges inMalaysia, Indonesia, the Philippines, and Singapore. ADBI Working Paper Series No. 288. https://www.adb.org/sites/default/files/publication/156143/adbi-wp288.pdf (accessed 15 September 2022). https://doi.org/10.2139/ssrn.1859991

Gale, B. 1981. Petronas: Malaysia’s national oil corporation. Asian Survey 21 (11): 1129–1144. https://doi.org/10.2307/2643998

Malaysiakini. 2019. Ten years before known oil, gas reserves run dry. Malaysiakini, 13 March 2019. https://www.malaysiakini.com/news/467781 (accessed 24 September 2022).

Menon, J. and Ng, T. H. 2017. Do state-owned enterprises crowd out private investment? Firm level evidence from Malaysia. Journal of Southeast Asian Economies 34 (3): 507–522.

Ministry of Finance Malaysia. 2022a. 2022 fiscal outlook and federal government revenue estimates. https://budget.mof.gov.my/pdf/2022/revenue/fiscal_outlook_2022.pdf (accessed 23 October 2022).

____. 2022b. Govt needs to implement expenditure saving measures, help subsidy costs. https://www.mof.gov.my/portal/en/news/press-citations/govt-needs-to-implement-expenditure-saving-measures-help-subsidy-costs (accessed 20 October 2022).

Petronas. 2019. Annual report 2019. https://www.petronas.com/sites/default/files/Media/PETRONAS-Annual%20Report-2019-v2.pdf (accessed 4 October 2022).

Rönnbäck, K., Broberg, O. and Galli, S. 2022. A colonial cash cow: The return on investments in British Malaya, 1889–1969. Cliometrica 16 (1): 149–173. https://doi.org/10.1007/s11698-021-00223-8

Salim, S. 2021. Dewan Rakyat passes second reading of bill to raise statutory debt limit to 65%. The Edge Markets, 11 October 2021. https://www.theedgemarkets.com/article/dewan-rakyat-passes-second-reading-bill-raise-statutory-debt-limit-65 (accessed 20 September 2022).

Tay, C. 2022. IMF ups Malaysia’s 2022 growth forecast to 5.4%, cuts 2023 projection to 4.4%, warns of global recession. The Edge Markets, 12 October 2022. https://www.theedgemarkets.com/article/imf-ups-malaysias-2022-growth-forecast-54-cuts-2023-projection-44-warns-global-recession (accessed 14 October 2022).

The Sun Daily. 2022. Experts: GST is great but fix problems before reintroduction. The Sun Daily, 10 June 2022. https://www.thesundaily.my/local/experts-gst-is-great-but-fix-problems-before-reintroduction-BB9311344 (accessed 6 October 2022).

Torii, T. 1997. The new economic policy and The United Malays National Organization—with special reference to the restructuring of Malaysian society. The Developing Economies 35 (3): 209–239. https://doi.org/10.1111/j.1746-1049.1997.tb00846.x

Ungku Abdul Aziz, U. A. H. 1970. Selected aspects of rural development in Malaysia. Bangkok: Economic Commission for Asia and the Far East.

Wicks, P. 1971. The new realism: Malaysia since 13 May, 1969. The Australian Quarterly 43 (4): 17–27. https://doi.org/10.2307/20634465

Worldometer. 2016. Malaysia oil. https://www.worldometers.info/oil/malaysia-oil/ (accessed 25 September 2022).

The World Bank. 2021. GDP growth (annual %) – Malaysia. https://data.worldbank.org/indicator/NY.GDP.MKTP.KD.ZG?locations=MY (accessed 15 September 2022).

____. 2019. Malaysia economic monitor June 2019: Re-energizing the public service. https://www.worldbank.org/en/country/malaysia/publication/malaysia-economic-monitor-june-2019-re-energizing-the-public-service (accessed 5 October 2022).

Yacob, S. 2021. PETRONAS, oil money, and Malaysia’s national sovereignty. Journal of the Malaysian Branch of the Royal Asiatic Society 94 (1): 119–144. https://doi.org/10.1353/ras.2021.0014

Yong, S. S. and Sia, J. K.-M. 2021. COVID-19 and social wellbeing in Malaysia: A case study. Current Psychology 2021. https://doi.org/10.1007/s12144-021-02290-6

Pritish Bhattacharya is Senior Research Officer in the Regional Economic Studies Programme at the ISEAS – Yusof Ishak Institute, Singapore. His research focuses on ASEAN’s development initiatives in the areas of trade, investment, and services. Pritish’s recent publications assess the impact of diverse public policies in the region, including those related to multilateral trade agreements, fiscal policy stabilisation, and post-pandemic growth strategies. His latest edited volume is titled The Comprehensive and Progressive Agreement for Trans-Pacific Partnership: Implications for Southeast Asia (ISEAS 2021). Since 2017, Pritish has been Associate Editor of the Journal of Southeast Asian Economies (JSEAE). Before joining ISEAS – Yusof Ishak Institute, he was a Research Assistant in the Department of Marketing at NUS Business School. Pritish has a Master’s Degree in Applied Economics from the National University of Singapore and a Bachelors (Hons) Degree in Economics from the University of Delhi. Email: pritish_bh@iseas.edu.sg.

Francis E. Hutchinson is Senior Fellow and Coordinator of the Malaysia Studies Programmes at the ISEAS – Yusof Ishak Institute, Singapore. He holds a PhD in Public Policy and Administration from the Australian National University and degrees from the Universities of Cambridge and Sussex. His research interests include governance, state-business relations, federalism, decentralisation, and industrialisation in Southeast Asia. He has written or edited five books including Asia and the Middle Income Trap (Routledge 2016); is the Managing Editor of the Journal of Southeast Asian Economies; and has published on Southeast Asian economic and political issues in Asian Affairs, Asian-Pacific Economic Literature, Journal of Contemporary Asia, Asian Journal of Political Science, Journal of the Royal Asiatic Society,and Southeast Asian Affairs. Prior to joining ISEAS – Yusof Ishak Institute, he carried out applied research for agencies such as the World Bank, UNDP, UNICEF, UNESCO, AusAID as well as political risk consultancy firms such as Oxford Analytica. Email: francis_hutchinson@iseas.edu.sg.